A Google SERP analysis of 228 apparel keywords reveals a counterintuitive Q1 2026 story: Shopping Ads as a SERP feature lost presence quarter-over-quarter, yet two very different brands, ultra-fast-fashion giant Shein and quality-first challenger Quince dramatically accelerated their share of that shrinking pie.

The Macro Picture: Shopping Ads Presence Is Slipping

Before looking at individual advertisers, the broader SERP landscape sets critical context. Across 20+ SERP features tracked on apparel keywords, the Shopping Ads widget saw its average daily presence dip from 1.19% in Q4 2025 to 1.16% in Q1 2026, a modest but directionally meaningful –2.4% decline quarter-over-quarter.

This matters because it signals that Google is surfacing Shopping Ads on fewer apparel queries than it was during the holiday season. The competitive real estate is contracting. Against this backdrop, any brand that grew its Share of Voice (SOV) wasn’t just holding steady, it was actively displacing competitors.

The Risers: Shein, Quince, and Prada Surge

Shein: Dominant at #1 with +81% SOV Growth

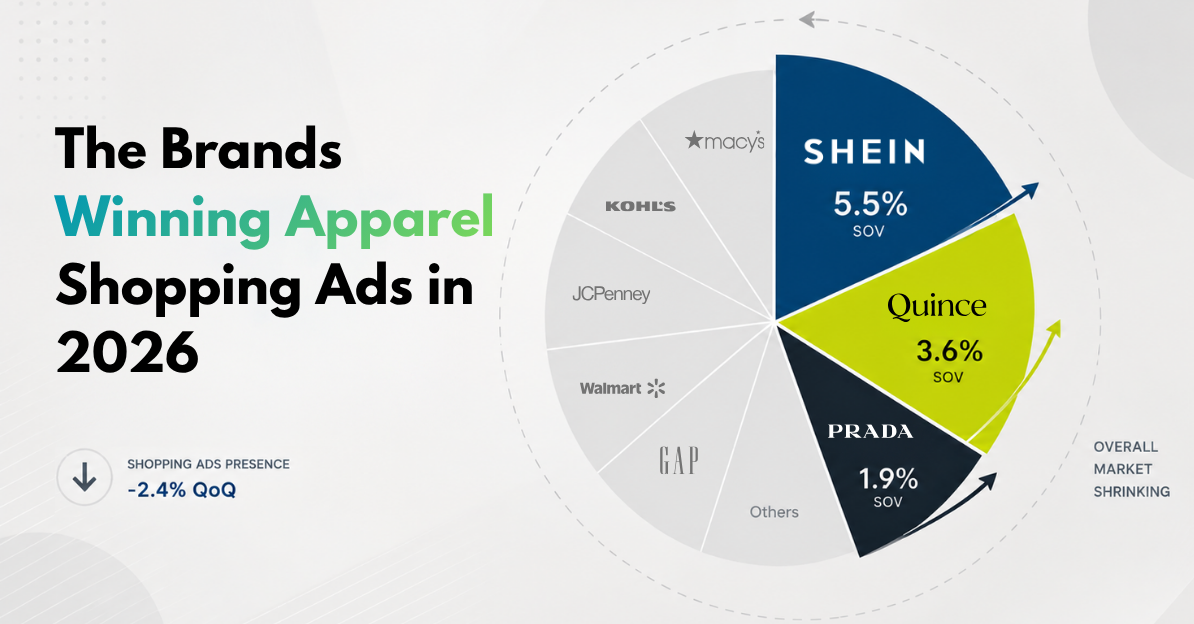

Shein entered Q1 2026 as the single largest force in apparel Shopping Ads, capturing 5.5% SOV across 228 tracked keywords, the highest of any advertiser in the competitive set. That’s up from 3.2% in Q4 2025, an +81% increase quarter-over-quarter.

What makes this particularly striking is that Q4 is historically the most competitive quarter for retail advertising, with holiday gifting season driving massive ad spend across the entire industry. Shein not only held its position through that pressure, it accelerated once the holiday season ended suggesting a deliberate, sustained investment rather than a seasonal spike.

Daily trend data reinforces the picture. Within Q1 itself, Shein showed a consistent upward trajectory month-over-month, with March delivering the strongest daily SOV figures of the entire quarter. The brand was actively increasing spend as Q1 progressed, not coasting on early momentum.

Read More: How TEMU is Challenging SHEIN’s Dominance in 2025

| Q4 2025 | Q1 2026 | Change | |

|---|---|---|---|

| SOV% | 3.2% | 5.5% | +81% |

| Rank | #3 | #1 | ↑ |

Quince: The Stealth Challenger at +149% Growth

If Shein’s growth is impressive, Quince’s is extraordinary. The brand went from 1.4% SOV in Q4 2025 to 3.6% in Q1 2026, a +149.2% increase that vaulted it from a mid-tier advertiser to the #2 position overall, ahead of established mass-market names like Target (1.9%) and Gap (1.7%).

Quince occupies the opposite end of the value spectrum from Shein. Where Shein competes on trend velocity and price, Quince positions itself on quality fabrics at transparent, factory-direct pricing, a direct challenger to brands like Everlane and accessible luxury labels. Its aggressive Shopping Ads investment in Q1 suggests it is deliberately converting organic brand awareness into paid search capture, meeting consumers who already know the brand and are now actively searching for specific products.

Like Shein, Quince’s daily trend data shows consistent month-over-month growth within Q1, with February and March both meaningfully stronger than January.

| Q4 2025 | Q1 2026 | Change | |

|---|---|---|---|

| SOV% | 1.4% | 3.6% | +149.2% |

| Rank | #12 | #2 | ↑ |

Prada: Luxury Enters the Format

Perhaps the most strategically significant riser is Prada, which grew its SOV from 0.87% to 1.9%, a +112.2% increase placing it 4th overall among all apparel Shopping Ads advertisers. Luxury brands have historically been reluctant to participate in Google Shopping due to brand perception concerns around price-comparison environments. Prada’s scaling Q1 presence suggests that calculation is changing.

Daily trend data makes Prada’s trajectory the clearest of the three: the brand was largely absent from Shopping Ads before late Q4 2025, then showed up consistently from December onward, with each month of Q1 stronger than the last.

| Q4 2025 | Q1 2026 | Change | |

|---|---|---|---|

| SOV% | 0.87% | 1.9% | +112.2% |

| Rank | #19 | #4 | ↑ |

The Fallers: Legacy Retailers Retreat

The flip side of the risers story is a broad pullback by traditional retailers and the scale of that retreat is what made room for Shein, Quince, and Prada to grow.

Children’s Place: The Starkest Reversal

Children’s Place fell from 3.9% SOV in Q4 2025, the #1 ranked advertiser that quarter to just 0.93% in Q1 2026, a collapse of –76.3%. The brand went from leading the entire competitive set to barely registering in the top 15. Its exit from the top spot created the most visible opening in the market, and Shein stepped directly into it.

Read More: How the Children’s Place Leveraged Advertising Strategy

The Bigger Brands Retreat

Children’s Place was not alone. Virtually every major traditional retailer dramatically pulled back Shopping Ads spend post-holiday:

| Advertiser | Q4 2025 SOV | Q1 2026 SOV | Change |

|---|---|---|---|

| Children’s Place | 3.9% | 0.93% | –76.3% |

| Macy’s | 2.0% | 0.13% | –93.7% |

| Kohl’s | 2.6% | 0.33% | –87.3% |

| JCPenney | 2.2% | 0.33% | –85.2% |

| Walmart | 0.80% | 0.13% | –84.3% |

The pattern is consistent: department stores, big-box retailers, and value-oriented apparel brands all treated Q4 as peak spend and wound down aggressively in Q1. This is partly structural, holiday demand drives seasonal ad investment but the magnitude of the pullback handed significant impression share directly to the brands that stayed active.

The Central Paradox: Growing SOV in a Shrinking Format

The Shopping Ads SERP feature appeared less frequently overall (–2.4% quarter-over-quarter) yet Shein and Quince dramatically increased the share of those impressions they captured.

This creates a compounding advantage. When Shopping Ads do appear on apparel queries, Shein and Quince are now the brands most likely to show up. The brands that retreated handed impression share at the exact moment those impressions were most contested.

The top three advertisers in Q1, Shein (5.5%), Quince (3.6%), and Target (1.9%) now command a disproportionate share of all apparel Shopping Ads visibility. In a format that is slightly contracting, concentration at the top is accelerating.

Key Takeaways

- Shopping Ads share is more concentrated than ever. The top two advertisers alone, Shein and Quince command 9.1% of all tracked apparel Shopping Ads SOV. The brands that went dark in Q1 are not just losing impressions today; they are ceding competitive positioning as the field consolidates.

- Post-holiday is not a time to go dark. The brands that pulled back handed impression share directly to more aggressive competitors. In an environment where Shopping Ads presence is already declining as a SERP feature, absence compounds quickly.

- All three risers accelerated within Q1 itself. This wasn’t a one-time step-change at the start of the quarter, Shein, Quince, and Prada each showed consistent month-over-month growth from January through March, meaning the gap between them and the retreating brands widened throughout the quarter.

- Luxury is no longer avoiding Google Shopping. If Prada can rank 4th in a broad apparel competitive set and grow every month within Q1, the historical reluctance of luxury brands to participate in this format appears to be ending.

Are Shopping Ads Dominating Your SERP?

Monitor shopping ads presence, track competitor SOV, and benchmark your brand across 12 markets and every major vertical with GrowByData.